KAST Card Review 2026: A Stablecoin-Native Card I Actually Use Daily

By an editor with 5+ years of fintech industry expertise · Updated May 2026 · ~15 min read

I’ve been running a KAST card alongside my Wirex for a couple of months now. Virtual K Card, Standard tier, used it across the UAE and Cyprus, paid for everything from ride-hailing to my Claude.ai subscription with it. Tap-to-pay through Apple Pay, online checkouts, the works.

Most KAST reviews you’ll find are written by people who topped up $50, took screenshots, and never touched it again. This one isn’t. I’ll show you exactly what the rewards look like in my account right now, explain the one thing about KAST’s reward system that nearly every other review gets wrong, and tell you honestly where it beats Wirex and where it doesn’t.

Best for: People who hold stablecoins (USDC/USDT) and want to spend them globally with the lowest friction, especially on USD-priced things, plus anyone who wants free exposure to KAST’s upcoming token via points.

Not for: Heavy ATM users (withdrawals are expensive), people who spend mostly in non-USD currencies (there’s an FX fee Wirex doesn’t charge), or anyone who wants self-custody.

My rating: 8/10 — A genuinely excellent stablecoin spending card with real USD cashback, a clean app, and broad global reach. Held back from a perfect score by FX fees on non-USD spend, expensive ATMs, and a points system whose real value won’t be known until a token launch that hasn’t happened yet.

Reader perk

Sign up with my link or code LBY9BQVJ and get 10% off a paid membership.

Is KAST the Right Card for You?

| Your situation | Best card |

|---|---|

| You hold USDC/USDT and want to spend globally with near-zero friction | KAST ✅ |

| You spend mostly in USD (online subscriptions, US merchants) | KAST ✅ |

| You want a free card with real USD cashback | KAST ✅ |

| You want free exposure to a crypto token airdrop | KAST ✅ |

| You spend mostly in non-USD local currencies and hate FX fees | Wirex (0% FX) |

| You want self-custody — no platform holds your keys | Avici or Bleap |

| You withdraw cash from ATMs frequently | Traditional bank card |

| You want maximum cashback and will stake $5K+ | Crypto.com Card |

KAST Card Fees, Limits & Quick Numbers

| Spec | Value |

|---|---|

| Annual fee (Standard) | $0 |

| USD cashback | 1.5% on first $2,000/month |

| Bonus rewards | KAST Points (toward future token) |

| FX fee (non-USD spend) | 0.5%–1.75% |

| FX fee (USD spend) | 0% |

| Stablecoin top-up | 0% (1:1 to USD) |

| Non-stablecoin deposit | 2%–5% conversion |

| ATM fee | $3 + 2% + operator fee |

| ATM limits | $250/withdrawal, $750/day |

| Card type | VISA Platinum (Standard) |

| Physical / Virtual | Both (2 free cards) |

| Apple Pay / Google Pay | Yes |

| Custody model | Custodial |

| Supported regions | 170+ countries |

| Inactivity fee | $1/mo after 12 months |

My Experience: A Couple of Months In

I added KAST mainly to have a stablecoin-native card sitting next to my Wirex. Where Wirex is my multi-currency travel card, KAST became my “spend my USDC stack” card. Same regions — UAE, Cyprus — same use pattern: online payments and Apple Pay everywhere.

What’s worked, plainly:

Stablecoin-to-spend is genuinely frictionless. You load USDC, the card draws from a USD balance, you tap to pay. No off-ramp, no “sell crypto, wait for bank transfer, then spend.” It’s the closest thing to spending stablecoins like a normal bank card that I’ve used.

Apple Pay just works. Added the virtual card to my wallet, tap-to-pay has been flawless across both countries. No re-auth nonsense.

The app is clean and fast. Transactions show up instantly. The freeze toggle is genuinely instant. The whole thing feels more modern than most crypto card apps, Wirex included.

It’s USD-denominated, which is the point. My balance is in dollars, my cashback is in dollars, and when I spend in USD (subscriptions, online services) there’s zero FX fee. For a stablecoin holder, that’s exactly the right design.

What annoys me, honestly

Very little — it does what I want. The only real friction is the ATM situation (more below), but since I don’t use KAST for cash withdrawals (that’s what other cards are for), it doesn’t bite me. If I’m being thorough: it’s a young product, and “young” always carries some risk I’ll cover in the honest section.

The Honest Catch: What Other Reviews Get Wrong

The things most KAST reviews either skip or get flat-out wrong.

1. The reward system: USD cashback (real) + Points (a bet) — and the rules just changed

This is the single most misunderstood thing about KAST, partly because the program keeps evolving. Here’s the honest, current picture as of May 2026.

You earn in two ways now:

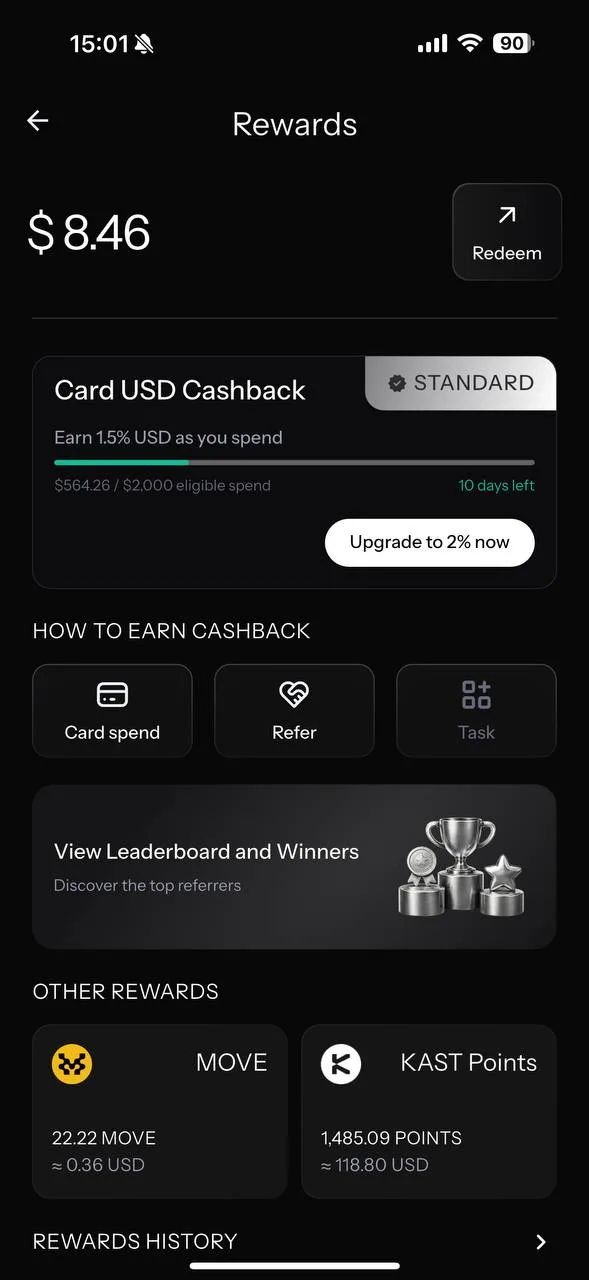

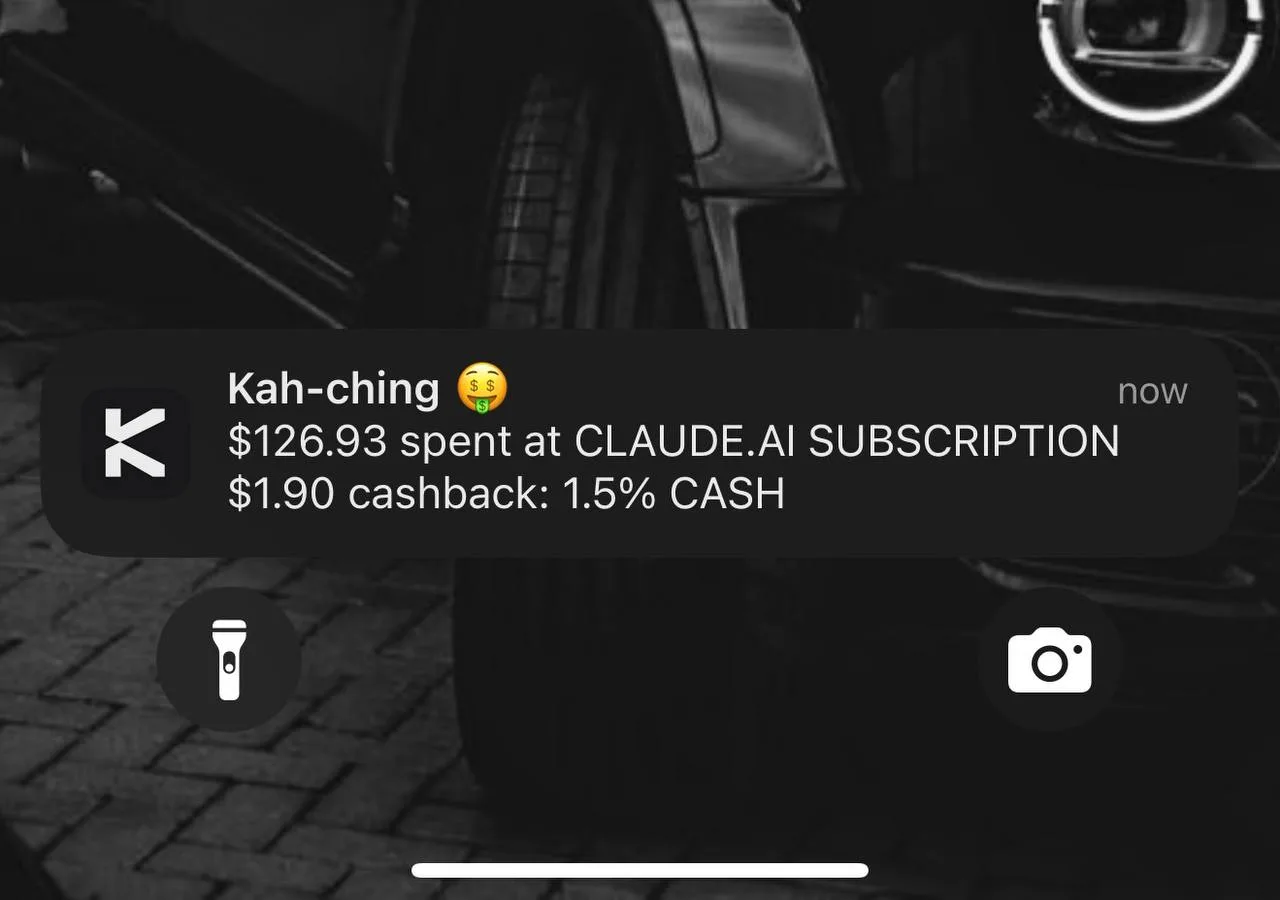

Stream 1 — USD Cashback (real money). On Standard, you earn 1.5% back in actual US dollars — but only on your first $2,000 of card spend per month. Spend beyond that in a month and the extra doesn’t earn cashback at the Standard tier. Here’s a notification from my phone the moment I paid for my Claude subscription:

That “$1.90 cashback: 1.5% CASH” on a $126.93 purchase is the real, no-asterisk reward. It lands in USD. One catch: it’s not auto-redeemed — you have to claim it in the Rewards Hub, and if a purchase is later refunded, the cashback can be clawed back.

Stream 2 — KAST Points (a bet, not cash). You also accumulate KAST Points. My account shows 1,485 points, which the app values at a “notional” $0.08 each — about $118.80. But that number deserves heavy skepticism, and here’s why most reviews never explain the fine print:

- Points can’t be converted until KAST launches its token (TGE), targeted for 2026 but “subject to regulatory approvals.” No token, no cash value.

- Even at TGE, you don’t get the full amount. You either convert 50% immediately and forfeit the other 50%, or convert 25% immediately with the rest dripping out monthly over 24 months. So that “$118.80” is realistically more like ~$59 instantly, or a two-year wait.

- Points can go up or down in value — the $0.08 is notional, not guaranteed.

- KAST can remove your points at its sole discretion, without explanation (their “Stop Misuse” clause).

- Some countries may be restricted from converting points to tokens at all.

So treat KAST Points as a free lottery ticket layered on top of the cashback — nice if it pays out, but not money you can count on. The real, bankable reward is the 1.5% USD.

A note on $MOVE

Until recently, KAST also paid a third reward — 4% back in $MOVE tokens (a Movement Labs partnership). That program has been discontinued — KAST paused $MOVE accruals when the partnership ended. I’d actually earned a decent stack while it ran (around 7,000 $MOVE, which I sold on Bybit). If you read older KAST reviews hyping “4% in $MOVE on top of everything,” know that it’s no longer active. This is a good example of why KAST’s rewards need an asterisk: the programs change.

2. There’s an FX fee — Wirex doesn’t have one

KAST charges 0.5%–1.75% on non-USD transactions (the exact rate depends on your residence and where you spend). If you spend in USD, it’s 0%. But if you’re buying things priced in EUR, GBP, or any non-dollar currency, you pay this fee.

This is a real difference from Wirex, which charges 0% FX across the board. For a stablecoin holder spending mostly in USD-priced things, KAST’s fee rarely bites. But if you’re a European spending euros daily, Wirex is cheaper on FX. Know your spending pattern.

3. ATM withdrawals are expensive and capped

If you’re thinking of KAST as a cash card — don’t. ATM withdrawals cost $3 flat + 2% of the amount, plus whatever the ATM operator charges. And they’re capped hard: $250 per withdrawal, 3 withdrawals per day, $750/day maximum.

Quick math: pull $250 out and you pay $3 + $5 = $8 minimum before the operator fee. That’s over 3% just to access your own cash. KAST is a spending card, not a cash card. Use something else for ATMs.

4. Funding with non-stablecoins costs you 2%–5%

If you deposit USDC or USDT, it converts 1:1 to your USD balance with zero spread — perfect. But if you deposit SOL, ETH, or BTC, KAST auto-converts it at a 2%–5% conversion fee before you can spend. On a $1,500 SOL deposit that’s $30–75 gone before your first purchase. The lesson: fund with stablecoins, not volatile crypto. Convert to USDC first, then load.

5. It’s custodial — and young

KAST holds your funds. You don’t have the keys — the card draws from a balance held by KAST’s licensed partners (the card is issued by Third National Bank; USD accounts are powered by Bridge via Lead Bank). This is standard for crypto cards, but it means standard custodial risk: keep only what you spend, not your savings.

It’s also a young product (KAST raised its $80M Series A in May 2026 and reports 1M+ users). Young means fast-moving and well-funded, but also less of a track record than a card like Wirex that’s been around since 2014. The reward programs change — as the $MOVE discontinuation shows. The token hasn’t launched. Factor that in.

Real Fees and Limits

| Fee | Amount |

|---|---|

| Annual fee (Standard) | $0 |

| Free cards | 2 (virtual or physical) |

| Extra virtual card | $2 each |

| Physical card shipping | $40 |

| Stablecoin top-up | 0% |

| Non-stablecoin deposit | 2%–5% |

| ACH deposit | $2 |

| FedWire deposit | $15 |

| FX fee (non-USD) | 0.5%–1.75% |

| ATM withdrawal | $3 + 2% + operator |

| Declined transaction | $0.50 |

| Inactivity (12mo+) | $1/month |

Spending limits: Card spending is effectively “up to whatever’s in your balance” — no artificial monthly spending cap, which is genuinely refreshing. (Note: the cashback is capped at the first $2k/month on Standard, but your actual spending isn’t limited.) ATM is the restrictive part: $250/withdrawal, 3/day, $750/day.

Stablecoin withdrawal network fees: Solana ($1 + 0.1%), Arbitrum ($0.20 + 0.1%), Ethereum ($6 + 0.1%), Tron ($5 + 0.1%). Solana is cheapest — fitting, since KAST is Solana-first.

Cashback Reality: What I Actually Earned

Let me give you the real numbers from my account, not marketing math. Over roughly two months on the free Standard tier:

$8.46 in USD cashback

Real, spendable, at 1.5%. This is the guaranteed floor — actual dollars.

1,485 KAST Points

Notionally ~$118.80, but realistically worth far less until (and unless) the token launches — and even then halved or stretched over 24 months. I count this as upside, not money.

How I cash out: Real USD cashback I redeem in-app. When the $MOVE program was still running, I withdrew those tokens straight to Bybit and sold them on the exchange — that’s how I turned that part of the rewards into spendable cash. With $MOVE now discontinued, the cashable reward today is the USD balance.

The realistic effective rate for a Standard user spending in USD is around 1.5% guaranteed (on the first $2k/month), plus whatever the Points eventually become. And critically, the guaranteed part is paid in dollars, not a volatile native token like Wirex’s WXT. That’s a real structural advantage: KAST’s base reward doesn’t depend on you holding and praying on a thin token.

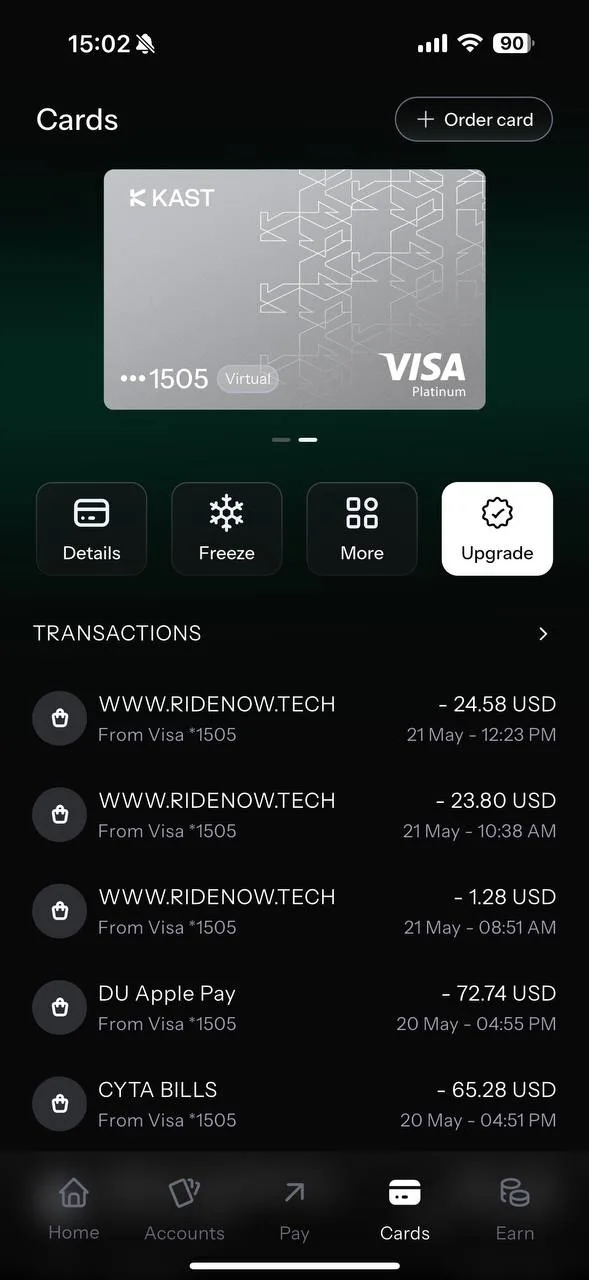

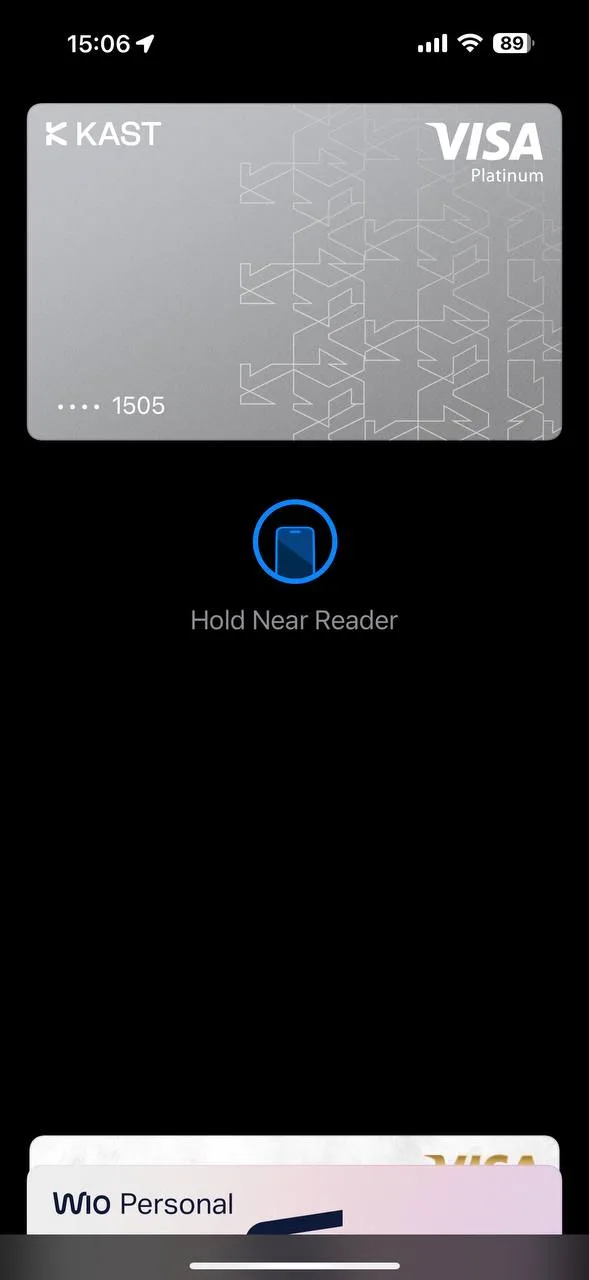

Card Format: Virtual-First, Apple Pay, Metal on Paid Tiers

On Standard, you get 2 free cards — virtual or physical — issued as VISA Platinum. I run mine entirely virtual and have never ordered the physical card, simply because I don’t need it: for online payments and Apple Pay, plastic is redundant. But the option is there. If you want the physical card, it comes out of your 2-card allowance plus a $40 shipping fee, and additional virtual cards beyond the free two are $2 each.

The virtual card drops straight into Apple Wallet (or Google Pay), and from there it’s tap-to-pay anywhere contactless is accepted. This is how I use it almost all the time — phone out, tap, done. Works identically to a normal bank card at the terminal.

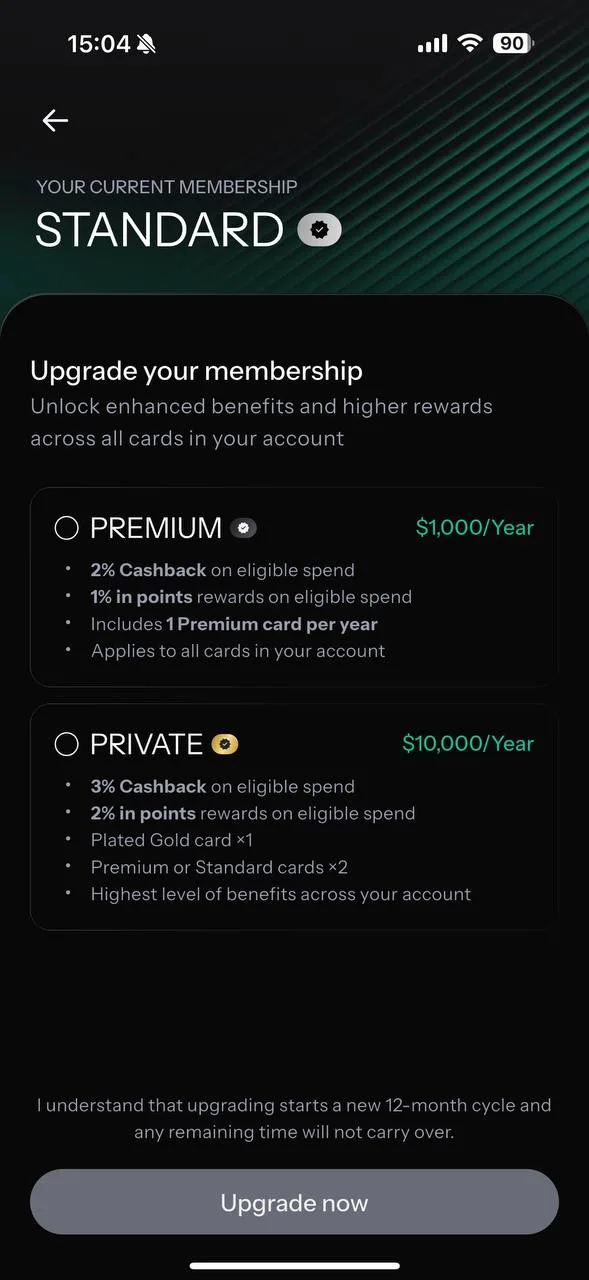

Want a metal card? That’s where the membership tiers come in:

- Standard (free) — virtual + physical option, 1.5% cashback on first $2k/month, VISA Platinum

- Premium ($1,000/year) — 2% cashback on first $10k/month + 1% in KAST Points on all spend, VISA Infinite, metal card

- Private ($10,000/year) — 3% cashback on first $40k/month + 2% in KAST Points on all spend, plated gold card

There are also fun card designs (Solana Card, Bitcoin Card, the Pudgy Penguins “Pengu Card”) — same economics, different looks. One catch on upgrading: the app warns that upgrading “starts a new 12-month cycle and any remaining time will not carry over.” So don’t upgrade mid-cycle expecting a pro-rated deal.

Is a paid tier worth it? For most people, no. On Standard, card-spend points only come on paid tiers — Standard’s points come mainly from referrals, onboarding, tasks, and optional SOL staking. The paid tiers add card-spend points and higher cashback caps, but quick math on Premium: you’d need very high monthly volume for the extra cashback to cover the $1,000 fee. Unless you’re a high-volume spender who also wants the metal card and status perks, Standard is the right call. I’m on Standard and have no plans to change.

Beyond the Card: The KAST Ecosystem

KAST isn’t just a card — it’s closer to a stablecoin-powered money app. Worth knowing what else is in the box, because it adds real value even if the card is your main reason for joining.

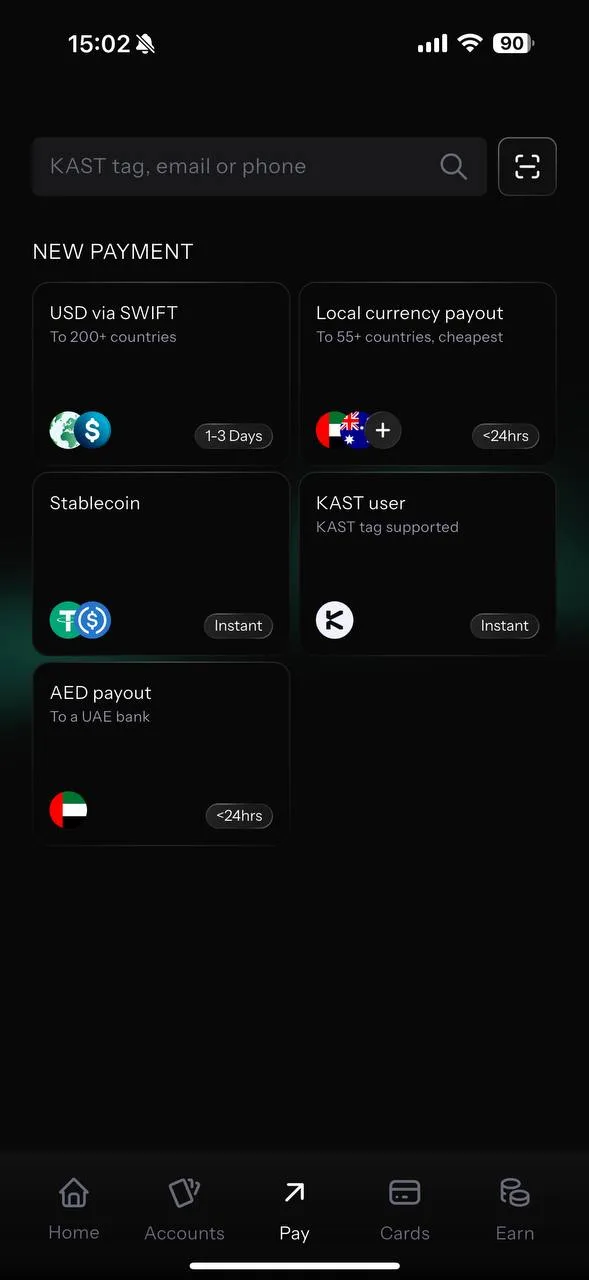

USD account with real bank details. You get a US account number and routing number without US residency — receive ACH payments, send wires, hold dollars. For freelancers and remote workers getting paid in USD, this is genuinely useful.

Global transfers. Send USD via SWIFT to 200+ countries, local-currency payouts to 55+ countries, instant stablecoin sends, or free instant transfers to other KAST users via KAST Tag.

KAST Earn. You can park stablecoins in yield vaults — a USD Prime Vault around 3.3% APY and a Gauntlet Alpha Vault around 4.3% APY. Not the highest yield in crypto, but it’s integrated and convenient if you’re already holding your spending balance there.

None of this is the reason to get KAST, but it’s why the product feels deeper than a standalone card. You’re getting a dollar account, transfers, and yield bundled with the spending card.

✅ Pros

- Free Standard tier — no annual fee, 2 free cards.

- 1.5% real USD cashback — paid in dollars, not a volatile native token. Big structural win over WXT-style rewards.

- Token upside via Points — a free bet on the upcoming $KAST token, layered on top of cash.

- 0% FX on USD spend and 0% stablecoin top-up — perfect for stablecoin holders.

- Frictionless stablecoin spending — load USDC, tap to pay, no off-ramp.

- Clean, fast app — instant transactions, instant freeze, modern UX.

- 170+ countries — broader reach than Wirex’s 35.

- Full ecosystem — USD account, global transfers, yield vaults bundled in.

- No spending cap — spend up to your balance.

❌ Cons

- Cashback capped — 1.5% only on the first $2,000/month on Standard.

- FX fee on non-USD spend (0.5%–1.75%) — Wirex charges 0%.

- Expensive, capped ATM — $3 + 2%, max $250/withdrawal, $750/day.

- 2%–5% fee funding with non-stablecoins — fund with USDC/USDT only.

- Points are uncertain — worthless until TGE (targeted 2026, not guaranteed), then halved or stretched over 24 months, and removable at KAST’s discretion.

- Reward programs change — the $MOVE token reward was discontinued; seasons and rates shift.

- Custodial — KAST holds your funds; not for self-custody purists.

- Young product — less track record than legacy cards.

Where KAST Stands Among Crypto Cards

KAST is a custodial, stablecoin-focused spending card — same category as Wirex, Avici, Bleap. Not an exchange card like Crypto.com or Binance. Here’s how it compares to the two cards I personally use alongside it.

KAST vs Wirex

I use both daily, so this is the comparison I know best.

Where KAST wins

- Real USD cashback (1.5% in dollars) vs Wirex’s 0.5% in volatile WXT

- 170+ countries vs Wirex’s 35

- Token upside via KAST Points vs Wirex’s nothing-extra

- Better app and UX — KAST feels more modern

- Bundled ecosystem — USD account, transfers, yield vaults

- Better Trustpilot — 3.3 vs Wirex’s 1.3

Where Wirex wins

- 0% FX on all currencies vs KAST’s 0.5%–1.75% on non-USD

- Free ATM allowance (€200/mo) vs KAST’s expensive capped ATM

- No $2k cashback cap — KAST’s 1.5% stops after $2k/month on Standard

- Track record — since 2014 vs KAST since 2024

- Multi-crypto — spend from 35+ coins vs KAST’s stablecoin focus

Use KAST if: You hold stablecoins, spend in USD, want real dollar cashback plus token upside, and value a modern app and broad country coverage.

Use Wirex if: You spend in many local currencies (0% FX matters), need free ATM withdrawals, or want the security of a card with a decade-long track record.

KAST vs Avici

Avici is self-custodial — you hold the keys, it’s a secured credit card on Solana. Fundamentally different model.

Where Avici wins: Self-custody (KAST can’t freeze what it doesn’t hold), 0% FX, Visa Signature perks for $30/year. Where KAST wins: Real cashback (Avici has 0% rewards), simpler UX, broader country coverage, the bundled ecosystem.

Use KAST if: You want rewards and convenience and are comfortable custodial. Use Avici if: Self-custody is non-negotiable and you don’t care about cashback.

What about Crypto.com, Binance, Coinbase cards?

These are exchange ecosystem cards — rewards come from staking the exchange’s native token (CRO, BNB). If you’re already deep in one of those exchanges, their card is a logical add-on. If you just want to spend stablecoins with the lowest friction and real dollar cashback, KAST is a cleaner answer that doesn’t require locking capital into a volatile exchange token.

Frequently Asked Questions

Is KAST a bank?

No. KAST is a financial technology company, not a bank. Cards, custody, and accounts are provided through licensed partners (the card is issued by Third National Bank; USD accounts run via Bridge and Lead Bank). Funds are not FDIC-insured as bank deposits — they’re a crypto-equivalent balance.

Is KAST safe?

KAST uses Sumsub identity verification, partners with Fireblocks and BitGo for security, and is backed by an $80M Series A (May 2026). No major fund-loss incidents reported. That said, it’s custodial and young — keep only your spending balance on it, not long-term savings.

What’s the difference between KAST cashback and KAST Points?

Two separate things. USD Cashback (1.5% on Standard, first $2k/month) is real spendable dollars. KAST Points are a farming reward valued notionally at $0.08 each, but they can’t be cashed until the $KAST token launches (TGE, targeted 2026), and even then you either forfeit half or wait up to 24 months for the full amount. Count the cashback as money; count the points as a bet.

What happened to the $MOVE rewards I read about?

KAST previously paid 4% back in $MOVE tokens through a Movement Labs partnership. That program has been discontinued. Older reviews citing “4% in $MOVE” are out of date. The current rewards are USD cashback plus KAST Points.

How do I cash out KAST rewards?

USD cashback is redeemed in the in-app Rewards Hub. KAST Points can’t be cashed until the token launches. (When the $MOVE program was active, those tokens could be withdrawn and sold on exchanges like Bybit — but that reward is no longer running.)

Does KAST charge FX fees?

0% on USD transactions. 0.5%–1.75% on non-USD transactions, depending on your region and where you spend.

Can I withdraw cash from ATMs?

Yes, but it’s expensive: $3 + 2% per withdrawal plus operator fees, capped at $250/withdrawal, 3/day, $750/day. KAST is best used as a spending card, not a cash card.

Is the free Standard tier enough?

For most people, yes. The paid tiers (Premium $1,000/yr, Private $10,000/yr) only make sense for very high-volume spenders who want metal cards, higher cashback caps, and card-spend points. I use Standard and see no reason to upgrade.

Which countries does KAST support?

170+ countries. It works anywhere Visa is accepted. A few markets have gaps and the available regions do change occasionally — check the app for your specific country before depositing.

Final Verdict

After a couple of months running it next to my Wirex:

KAST is the best stablecoin-native spending card I’ve used.

Load USDC, tap to pay anywhere, earn real dollars back — it nails the core job better than anything else in its category. The fact that the base cashback is paid in actual dollars rather than a thin native token is a genuine structural win over older cards like Wirex.

It’s not perfect. The FX fee on non-USD spend means it’s not the universal travel card Wirex is. The ATM economics are bad. The cashback caps at $2k/month on Standard. And the KAST Points — while a nice free bet — shouldn’t be counted as real money until the token actually launches and you see what it converts to. The recent discontinuation of the $MOVE reward is a useful reminder that these programs shift under your feet.

→ KAST is excellent. Get it.

→ Wirex’s 0% FX probably wins.

→ Avici or Bleap, not KAST.

→ None of these; use a bank card for ATMs.

My Rating

8/10

Higher than Wirex’s 7/10 in my book — better cashback (real dollars vs volatile token), far better Trustpilot, broader reach, deeper ecosystem, and a notably more modern app. Held back from higher by the non-USD FX fee, expensive capped ATM, the $2k/month cashback cap, the custodial model, and a points system whose value is still a promise rather than a payout.

If you spend stablecoins and want them to behave like real money with real rewards, KAST is one of the strongest options on the market right now — and it’s free to start.

Use code LBY9BQVJ for 10% off a paid membership.

This review reflects my personal experience as a KAST Standard user. Fees, limits, reward rates, and tier structures are accurate as of May 2026 and are subject to change — KAST’s reward programs in particular change periodically (the $MOVE reward, for example, was discontinued), so verify current terms at kast.xyz before signing up. KAST is a custodial product and a young company; only keep funds you actively spend. This article contains affiliate links — if you sign up via my link I may earn a commission at no cost to you. It doesn’t change my assessment, which is based on actual daily use.