Wirex Card Review 2026: 5 Years In, Here’s My Honest Take

By an editor with 5+ years of fintech industry expertise · Updated May 2026 · ~18 min read

I’ve held a Wirex Standard card since 2021. Used it across UAE, Russia, Ukraine, Kazakhstan, Armenia, Cyprus, and a half-dozen European cities. Cashed out from ATMs. Paid via Apple Pay and Apple Watch. Never had an account freeze. Never had a withdrawal blocked. Never paid a monthly subscription.

Most Wirex reviews run on a press kit and a 3-day test drive. This one runs on five years of actual transactions.

Best for: Frequent travelers who want a free debit card with zero FX fees, native crypto integration, and don’t care much about cashback rates.

Not for: People chasing high cashback. Despite Wirex’s “up to 8% Cryptoback” marketing, the Standard plan pays 0.5% — and the 8% tier has a hidden monthly cap most reviews don’t mention.

My rating: 7/10 — Reliable as a travel utility card, weak as a rewards play, and Trustpilot’s 1.3-star aggregate score deserves a serious conversation later in this review (it’s not what you think, but it’s also not nothing).

Is Wirex the Right Card for You?

Skip the rest of this review if you fit one of these clear “yes” or “no” cases:

| Your situation | Best card |

|---|---|

| You travel internationally often and want zero FX fees | Wirex ✅ |

| You hold crypto in multiple coins (BTC, ETH, USDT, etc.) and want to spend any of them | Wirex ✅ |

| You want a free card with no monthly fee and basic crypto integration | Wirex ✅ |

| You live primarily in stablecoins (USDC/USDT) and want broader country coverage | KAST (see comparison) |

| You want self-custody — no platform holds your keys | Avici or Bleap |

| You want maximum cashback (5%+) and willing to stake $5K+ in exchange tokens | Crypto.com Card |

| You’re in the United States | Coinbase Card |

| You want a no-fee card and don’t care about crypto rewards | Traditional bank card or Revolut |

If you fit the “Wirex ✅” rows, keep reading — the rest of this review explains why and shows you what to expect. If you fit one of the alternative rows, jump to the comparison section below for honest tradeoffs against your better option.

Quick Numbers (Standard Plan, EEA)

| Spec | Value |

|---|---|

| Monthly fee | €0 |

| Card issuance | Free |

| Cashback (Cryptoback™) | 0.5% in WXT |

| FX fees | 0% |

| Free ATM withdrawals | €200/month |

| ATM fee after free limit | 2% |

| Daily cash withdrawal limit (EEA) | €500 |

| Monthly cash withdrawal limit (EEA) | €5,000 |

| Daily purchase limit | €30,000 (per transaction & per day) |

| Monthly purchase limit | €30,000 (Virtual/Plastic) · €75,000 (Metal) |

| Bank transfer (SEPA) | €50,000/day |

| Supported cryptos | 35+ (BTC, ETH, USDT, USDC, more) |

| Apple Pay / Google Pay | Yes |

| Custody model | Custodial |

| Available regions | 35 countries |

Numbers above are from my own EEA-region Wirex app on May 2026. Limits vary by region — Wirex’s own documentation flags this explicitly. UK users get GBP equivalents (£500/day, £200/month free ATM). Singapore and APAC have separate SGD limits. Check your specific region’s limits inside the app before assuming the numbers above apply to you.

My 5-Year Experience: What Actually Happened

I signed up in 2021 because I wanted one card that worked the same way whether I was in Limassol, Dubai, or Kyiv. Five years later, I’m still using it for exactly that.

Here’s what’s worked, in plain terms:

Cash withdrawals abroad have always cleared. ATMs in seven different countries, no card freezes, no “verify your transaction” panic emails when I’m standing at a kiosk in Sharjah. The €500/day EEA cash limit isn’t generous, but it’s enough for hotel deposits, restaurant cash, or topping up at a casino. Crypto cards from competitors often have lower limits or none at all — Wirex hits a workable middle ground.

Apple Pay and Apple Watch work end-to-end. Added the virtual card to Apple Wallet years ago and tap-to-pay has just worked. No re-authentication every two weeks, no “card declined” surprises at metro turnstiles. This sounds basic until you’ve used a crypto card where the Apple Pay integration was an afterthought.

KYC was painless for me. Five years ago verification took maybe 5 minutes — passport photo, selfie, done. They’ve tightened it since (more on that in the next section), but for users who get in clean, the friction is low.

Support is decent when you need it. I haven’t needed it often, but when I’ve pinged the Wirex Private chat, response was usually under 30 minutes during UK business hours.

What annoys me, honestly

The €500/day cash withdrawal limit is the one thing I’d change. There’ve been times I needed €1,000+ in cash same-day and had to plan ahead by withdrawing across two days. For a card I’ve used for five years, I’d expect higher limits at this point — but Wirex doesn’t reward tenure with elevated limits, only with paid tier upgrades.

Beyond that? Honestly, nothing meaningful. The card is boring. It just works. In crypto, boring is a feature.

The Honest Catch: What Other Reviews Don’t Tell You

Five things most Wirex reviews bury or skip entirely.

1. The “8% cashback” is theatre for Standard users

Every Wirex marketing page mentions “up to 8% Cryptoback™.” It’s technically true. It’s also nearly impossible to actually earn 8%.

Here’s the breakdown:

- Standard (free): 0.5% cashback

- Premium ($9.99/month): ~1.5% cashback

- Elite ($29.99/month): Up to 8% cashback — but only with substantial WXT token holdings locked

To actually hit the 8% tier you need to subscribe to Elite and stake meaningful amounts of WXT tokens. The marketing literature for the top headline rate references holdings in the millions of WXT, which translates to thousands of dollars locked up just to qualify.

And here’s the cap that nobody talks about — your Cryptoback is capped at 10,000 WXT per month. At current WXT prices (~€0.00216 per token), that’s about €21.60/month maximum cashback regardless of how much you spend or what tier you’re on.

Translated: Even an Elite subscriber with full WXT staking, paying $29.99/month for the privilege, caps out at €22 worth of cashback monthly. That’s not a rewards card. That’s a subscription that pays you back ~€22 if you max it out.

2. WXT volatility is a real risk — but there’s a simple workaround

Cashback is paid in WXT, Wirex’s native token. WXT price has been volatile over the years — it’s an exchange-controlled token, not a major cryptocurrency. Holding WXT long-term is essentially a bet on Wirex’s business performance.

What I do: when WXT accumulates to a reasonable amount, I convert it to USDT inside the Wirex app (Exchange button on the WXT screen), then spend USDT as needed. No long-term WXT exposure. The token risk goes from “real concern” to “ignorable” if you treat WXT as an intermediate currency, not a holding.

Most reviewers don’t explain this. They just say “rewards in WXT, volatile” and move on. The volatility doesn’t matter if you convert weekly.

3. About that 1.3-star Trustpilot rating

Wirex’s Trustpilot score is currently 1.3 out of 5, with 94% of reviews being 1-star. That’s bad. Significantly worse than peers — Revolut sits at 4.3, Wise at 4.3, Crypto.com at 4.2. Even other custodial crypto cards rate 3-4 stars on average. Wirex’s 1.3 is an outlier even within the financial-services category, which already skews negative due to selection bias (people who get burned write reviews; satisfied users don’t).

So what’s actually going on? After reading through hundreds of recent negative reviews, three patterns emerge:

Pattern 1: Mass re-verification of dormant accounts (2024-2026)

Under increased compliance pressure from the UK FCA and EU regulators, Wirex pushed a massive re-verification wave. Users who hadn’t logged in for 1-2 years found their accounts either closed outright or requiring new passport KYC before any access. The wave hit at scale — when a platform closes tens of thousands of dormant accounts in a short window, all of those users have intense motivation to leave a 1-star review at once. Trustpilot ratings absorb that hit.

My personal experience with re-verification

When the prompt hit my account, I submitted current passport documents promptly — within 24 hours. My account stayed active. Nothing was lost, no access disrupted beyond the brief verification window. The users who got burned were either dormant for years and didn’t respond to the verification requests in time, or had documents from jurisdictions where additional checks couldn’t easily be cleared. If you’re an active user who treats verification requests as something to handle the same day they arrive, you’ll be fine.

Pattern 2: Slow “defund process” for closed accounts

When Wirex closes an account, returning the user’s funds (the “defund process”) can take weeks or months. The complaints are remarkably consistent: standard template responses (“we still have no updates”), no clear timeline, money inaccessible. This is the most legitimately concerning category of complaints — it’s not about the card not working, it’s about getting your money back when things go sideways.

Pattern 3: Compliance friction for users in flagged jurisdictions

Users with passports from sanctioned or high-risk regions (Russia and some others post-2022) face additional verification requirements, longer review times, and occasionally outright rejection. This is industry-standard compliance behavior, but Wirex’s communication during these reviews is, by user accounts, opaque and slow.

What this means for you, practically:

If you’re an active user with current KYC, you’re likely fine. My 5 years without a single issue isn’t an anomaly — it’s the median experience for actively-used accounts.

If you’re considering opening a new account today, here’s what reduces your risk:

- Complete full passport KYC immediately during signup. Don’t delay.

- Verify your address with a recent utility bill if requested.

- Use the card at least once a month. Dormancy seems to draw compliance scrutiny.

- Don’t keep significant balances on the card. Treat it as spending money, not savings.

- Keep your contact info current — if Wirex needs to reach you for compliance, you want to receive it.

- If you get a re-verification prompt, respond within 24-48 hours. This is the single biggest factor in whether re-verification goes smoothly or your account gets locked.

If you’re a returning user with a dormant account from years ago — expect friction. You’ll likely need full re-verification with current documents. Budget time and patience for it.

The bottom line: Trustpilot’s 1.3 isn’t ignorable, but it also doesn’t predict your experience as a new, actively-used account. It tells you about the tail risk (what happens if something goes wrong) more than the median experience (what happens day-to-day). Decide accordingly.

4. RF passport holders should expect extra verification

I’ve had friends with Russian Federation passports go through Wirex KYC, and they consistently faced longer verification timelines and additional document requests compared to users with EU/UK passports. They were eventually approved, but the friction is real.

This isn’t unique to Wirex — most regulated financial platforms have applied enhanced compliance checks to certain jurisdictions since 2022. But you should expect days, not minutes, for verification if you’re applying with a Russian-issued document. Be patient, respond to all document requests promptly, and don’t open multiple accounts trying to “speed it up” — that triggers worse outcomes.

5. It’s custodial, not self-custody

Wirex holds your crypto. You don’t have private keys. This isn’t a bug — most crypto debit cards work this way. But if you specifically want self-custody (you hold the keys, no platform can freeze funds), Wirex isn’t the answer. Self-custody alternatives exist and I’ll mention them in the comparison section below.

The trade-off: custodial = easier UX, regulated platform, support exists. Self-custody = no platform freeze risk, but no support, technical complexity, and your responsibility if you lose access.

I’m comfortable with custodial for spending money (small balances I’m actively using). I wouldn’t park my long-term holdings in any custodial card platform — Wirex included.

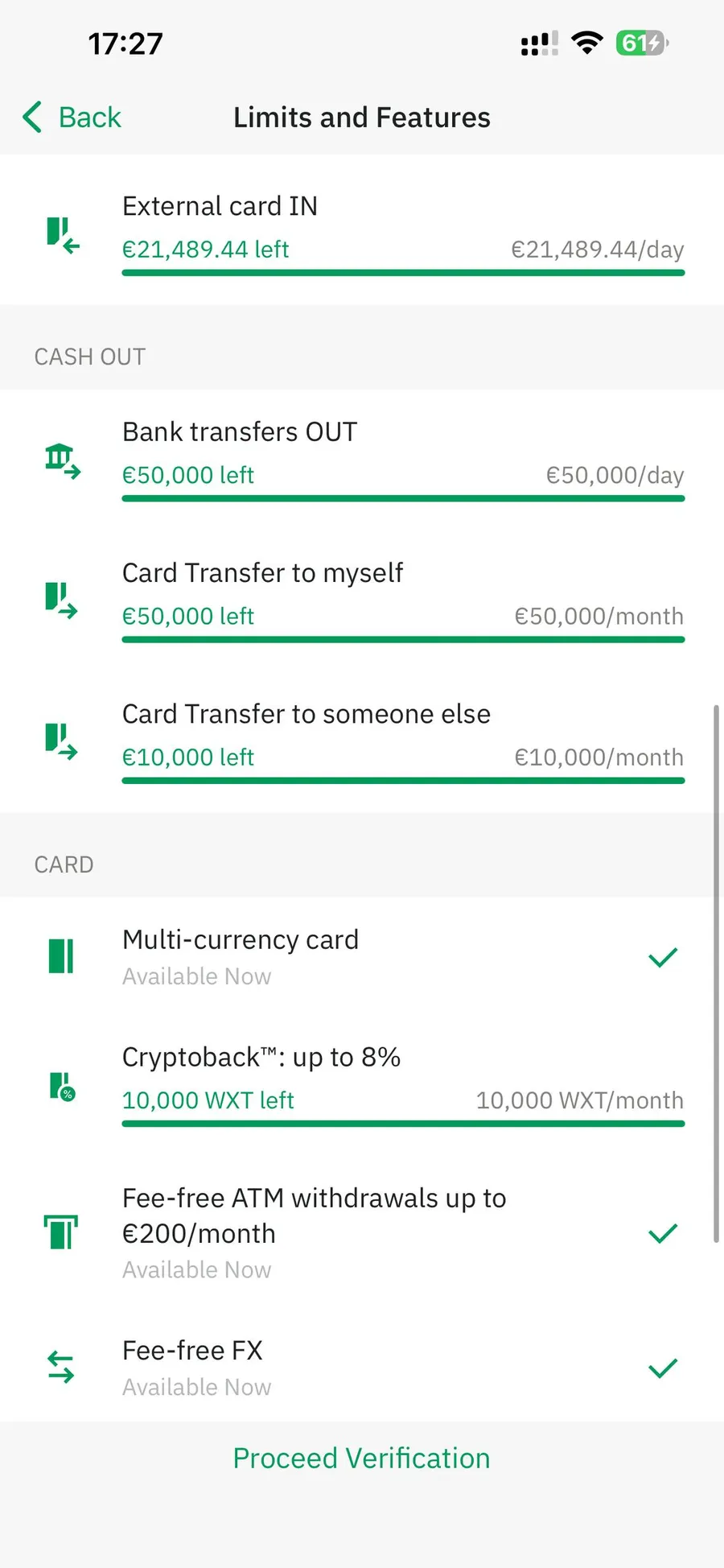

Wirex Fees and Limits — In-App, Right Now

Most reviews quote marketing pages. Here’s what my actual Wirex app shows me as a Standard user in EEA (May 2026):

Card features (Available now, Standard tier):

- Multi-currency card ✅

- Cryptoback 0.5% (up to 10,000 WXT/month — the cap I mentioned above)

- Fee-free ATM withdrawals up to €200/month

- Fee-free FX

- Apple Pay / Google Pay

Card limits (EEA region):

| Limit | EEA | UK | APAC | AU |

|---|---|---|---|---|

| Max purchase per transaction | €30,000 | £30,000 | 20,000 SGD | 20,000 AUD |

| Max purchase per day | €30,000 | £30,000 | 20,000 SGD | 20,000 AUD |

| Max purchase per month | €30,000 (V/P) · €75,000 (Metal) | £30,000 (V/P) · £75,000 (Metal) | — | — |

| Max purchase per 3 months | €75,000 | £75,000 | — | — |

| Max purchase per 6 months | €100,000 | £100,000 | — | — |

| Max cash withdrawal per day | €500 | £750 | 1,400 SGD | 1,400 AUD |

| Max cash withdrawal per month | €5,000 | £5,000 | 5,000 SGD | 5,000 AUD |

| Max cash withdrawal count per day | 5 | 5 | 5 | 5 |

Metal card monthly limits can be increased on request. All limits vary by region, currency, and verification level — check current limits in the Wirex app.

Transfer limits:

- SEPA Transfer (EUR): Up to €50,000/day

- Faster Payments (GBP): Up to £50,000/day

- Card-to-card (own card): €50,000/month

- Card-to-card (someone else): €10,000/month

- External card top-up (confirmed): $25,000/day

- External card top-up (unconfirmed): $15,000/day

These are real numbers from the app, not Wirex marketing. They confirm Wirex isn’t a card for people moving six-figure monthly volumes — but for normal spending and travel, the limits are workable.

On fees beyond the listed:

- Card-to-card transfer to third parties: 1% (subject to minimums)

- Crypto-to-fiat conversion spread: ~0.5% on common pairs (BTC, ETH, USDT/EUR)

- External card top-up fee: 0% for SEPA/bank transfer, 1.5%-2% for credit card top-up (varies by region)

The hidden fee that matters

When you spend with crypto at point-of-sale, Wirex converts at “its rate” which sits about 0.5% below mid-market. On a €100 transaction paid from BTC, you actually use €100.50 worth of BTC. This isn’t unique to Wirex (Crypto.com Card, Coinbase Card, Binance Card all do the same), but it’s a real cost that’s missing from the headline “0% FX” claim.

The workaround: pre-load the local fiat currency you spend most often. If you live in EEA, top up EUR. If you travel to GBP areas, hold some GBP. Spending from fiat balance bypasses the conversion spread entirely.

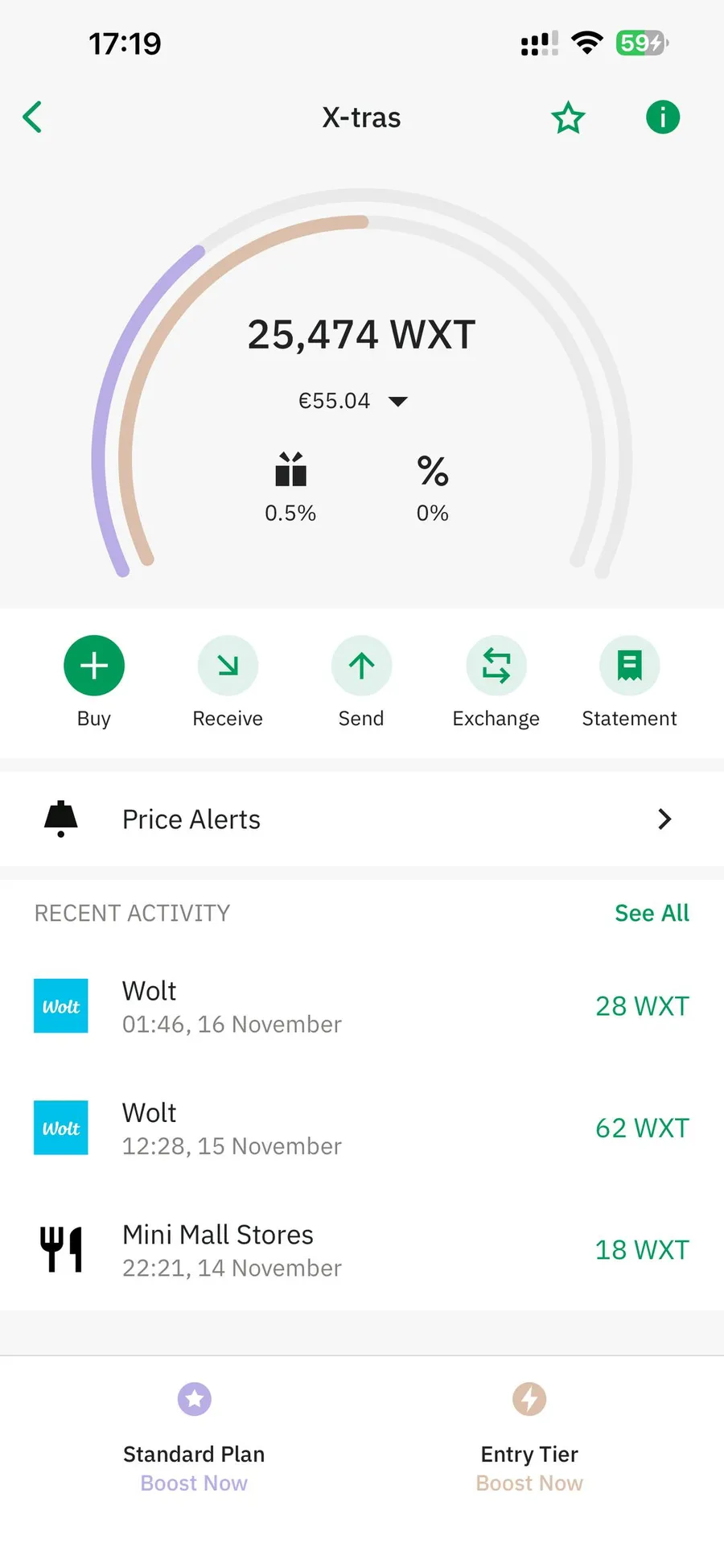

Cashback Reality Check

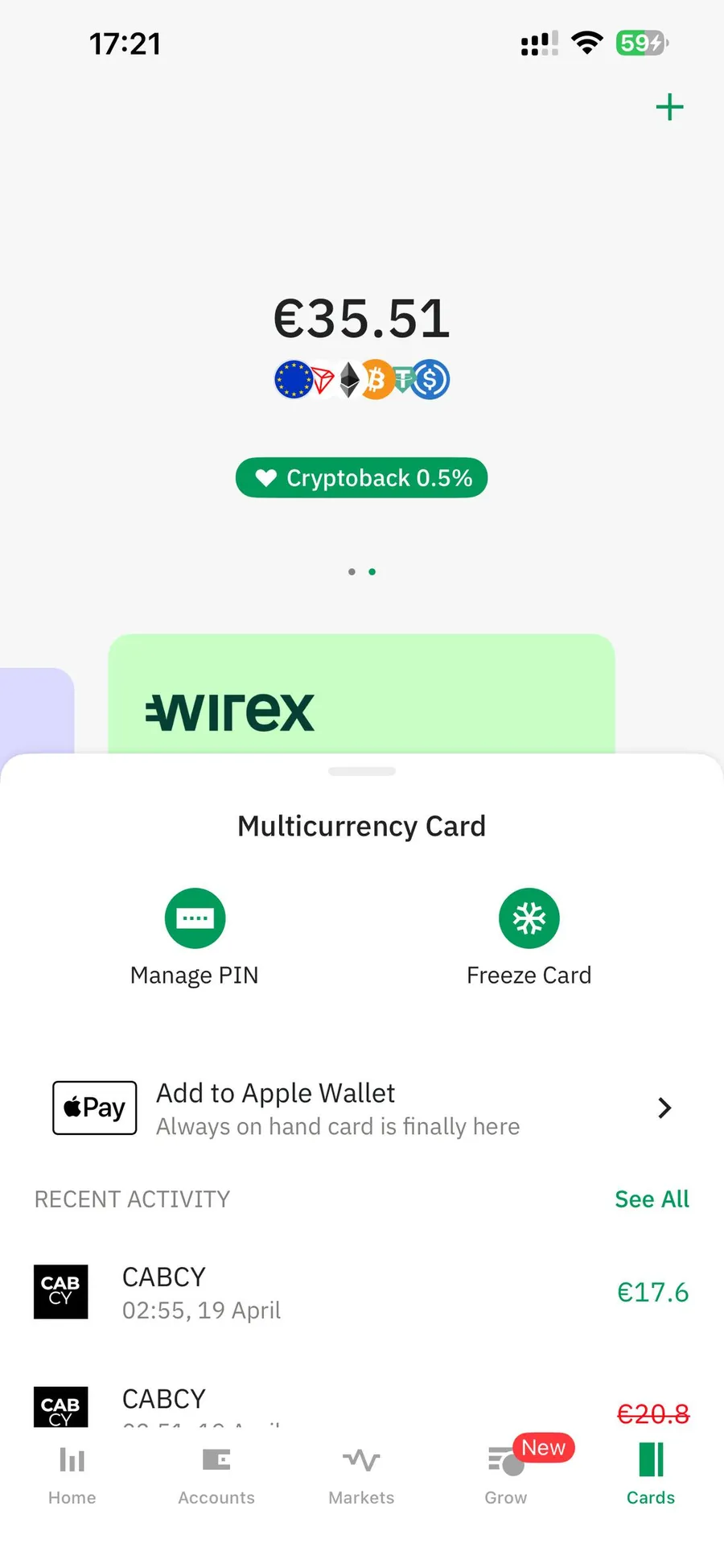

Let me show you what Standard-tier cashback actually looks like in the app, not in marketing copy.

That’s the app showing 0.5% Cryptoback on my Multicurrency Card screen. Not “up to 8%.” Just 0.5%, which is the realistic rate for Standard users.

My current WXT balance sitting in the X-tras section is 25,474 tokens — about €55 at today’s prices. That’s what I haven’t yet converted to USDT and spent. Over the years I’ve converted larger amounts to USDT periodically and used them for normal spending, so the historical total is higher — but the point isn’t the running total. The point is the rate.

At 0.5% on Standard, cashback compounds slowly. For someone spending €1,000/month on the card, you’re earning roughly €5/month in WXT — call it €60/year, less if WXT price drops. That’s the realistic Standard-tier number. Marketing claims of “up to 8%” simply don’t apply at this tier, regardless of how long you hold the card.

Should you be discouraged by this? Honestly, it depends on what you’re optimizing for:

If you wanted a cashback card

Yes, be discouraged. Wirex Standard is not your card. The cashback economics on Wirex Standard don’t compete with cards purpose-built for rewards (more on alternatives below).

If you wanted a travel-friendly free debit card with crypto integration

No, don’t be discouraged. The cashback is a small bonus. The real value is the 0% FX fees, which save you 1.5-2.5% on every foreign purchase compared to a typical bank card. For someone spending €2,000/month internationally, that’s €30-50/month in saved FX fees — and the savings come from a card that costs nothing to hold.

My math

~€5-10/month in WXT cashback + ~€40-60/month in saved FX fees (rough estimate based on my international spending) = Wirex Standard is paying me €500-700 annually to use it as my travel card. That’s why I haven’t switched.

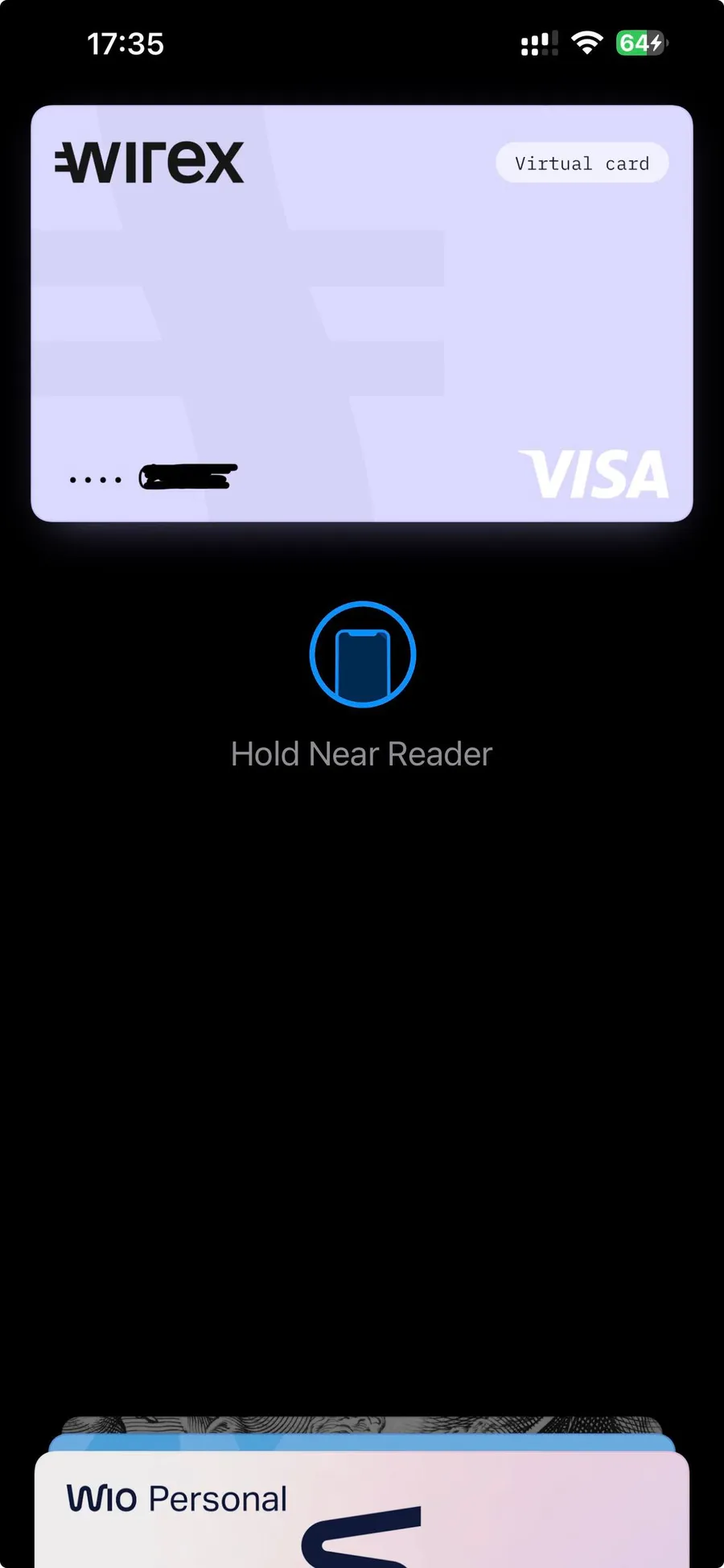

Card Format: Physical Visa, Virtual, Apple Pay Ready

Wirex Standard issues both physical and virtual cards. Both are Visa debit (not Mastercard, though some older regional editions did use Mastercard — current new issuances are Visa in most regions, per Wirex’s current website).

The physical card is contactless (tap-to-pay), looks like a normal debit card, and works anywhere Visa is accepted. I’ve used mine at corner shops in small towns and on hotel POS systems in Dubai — universal acceptance.

The virtual card lives in the Wirex app and can be added to Apple Wallet, Google Pay, or Samsung Pay. Once it’s in your wallet, you tap your phone/watch to pay just like a regular bank card.

What I appreciate about the dual format: if my physical card is lost or compromised, I freeze it in the app and keep paying via the virtual card on my phone. Continuity matters when you travel.

One thing to verify by region: physical card delivery times. Wirex states it ships physical cards within 7-14 days in most regions, but actual delivery varies significantly by country. If you need a physical card by a specific date, order it well in advance.

✅ Pros

- Free card, free account. No issuance fee, no monthly fee, no annual fee on Standard.

- 0% FX fees. Huge advantage over traditional bank cards (1.5-2.5% typical FX markup) for travelers.

- Multi-currency support. Hold and spend in 12+ fiat currencies, 35+ cryptocurrencies, with auto-conversion at point of sale.

- Apple Pay / Google Pay end-to-end. Add virtual card to mobile wallets, tap-to-pay works seamlessly.

- Global availability. 35+ countries, including most of EEA, UK, APAC, and select markets in Latin America.

- Reliable for daily use. In five years of personal use, no account freezes, no failed transactions abroad, no withdrawal blocks.

- Decent support response. Wirex Private chat typically responds under 30 minutes during UK business hours.

- Long operating history. Wirex has been issuing crypto cards since 2014 — longer than most competitors have existed.

❌ Cons

- Cashback is theatre on Standard. 0.5% in WXT is barely a perk. The “up to 8%” marketing requires Elite tier subscription + significant WXT staking, and is capped at 10,000 WXT/month regardless of spending.

- Custodial, not self-custody. Wirex holds your keys. Standard for crypto cards, but a limitation for users who specifically want self-custody.

- Trustpilot 1.3 rating reflects real (if narrow) issues. Re-verification waves, slow defund processes for closed accounts, and compliance friction for flagged jurisdictions are documented patterns.

- Cash withdrawal limits are modest. €500/day in EEA isn’t generous for users with significant cash needs.

- Conversion spread on crypto-to-fiat (~0.5%) is a hidden cost that the headline “0% FX” doesn’t capture.

- WXT rewards have volatility risk — though this is manageable by converting WXT to USDT periodically.

- No US availability. Wirex doesn’t operate in the United States.

- No physical card in some regions. Virtual-only in certain APAC markets.

Where Wirex Stands Among Crypto Cards

Here’s how Wirex fits the broader market — the honest answer always depends on what you’re optimizing for.

Wirex is a personal-spending custodial debit card with a strong travel focus. That puts it in direct competition with cards like KAST, Avici, Bleap, and Bybit Card — all of which target similar users (individuals who want to spend crypto on everyday purchases). It’s NOT in the same category as exchange-issued cards like Crypto.com Card, Binance Card, or Coinbase Card, which are bonuses tacked onto trading accounts and have fundamentally different economics around token-staking rewards.

I personally use two other cards alongside Wirex, so my comparison set is shaped by real day-to-day testing, not feature lists:

Wirex vs KAST Card

KAST is a newer entrant (launched in 2024, raised $80M Series A in May 2026). It’s a custodial Visa card focused on stablecoin spending — load USDC/USDT, the card draws from that balance. Where Wirex supports 35+ cryptocurrencies for top-up, KAST is essentially USD-stablecoin-only at point of sale.

Where KAST wins

- 170+ countries supported (vs Wirex’s 35)

- Token launch potential — KAST Points convert 1:1 to $KAST at TGE (Q4 2026)

- Higher headline cashback tiers — 2% base, up to 12% on Luxe

- No tier subscription required for base cashback

Where Wirex wins

- 0% FX fees (KAST charges 1.125% FX on non-USD)

- Longer track record — Wirex since 2014 vs KAST since 2024

- Multi-crypto support — spend from any of 35+ currencies, not just stablecoins

- Free ATM withdrawals (Wirex €200/mo free; KAST charges $3+2% on all)

Use Wirex if: You want one card that handles multi-currency travel spending in EU/UK/APAC and 0% FX matters more than cashback.

Use KAST if: You spend primarily in stablecoins, live outside Wirex’s supported regions, or want exposure to a token launch.

Wirex vs Avici Card

Avici is a fundamentally different beast — it’s a self-custodial Visa secured credit card built on Solana smart contracts. You hold the keys. Avici doesn’t hold your USDC; it’s collateralized in a smart wallet you control.

Where Avici wins

- Self-custody. Avici cannot freeze your funds. If you experienced FTX or Celsius collapses, this model is structurally safer.

- Visa Signature perks for $30/year — lounge access, travel insurance, $0 ATM fees

- 0% FX fees (matches Wirex)

- No platform-level compliance freezes

Where Wirex wins

- 0% cashback on Avici — no rewards program. Wirex’s 0.5% on Standard is still more than nothing.

- Broader regional availability (Wirex 35+ countries, Avici 48 but with different gaps)

- Multi-crypto support (Wirex 35+ currencies; Avici USDC-focused)

- Simpler UX — Wirex feels like a normal banking app

Use Wirex if: You want a “set it and forget it” card with reasonable rewards and no need to manage smart wallets.

Use Avici if: Self-custody is non-negotiable, you’re comfortable with on-chain mechanics, or you want premium Visa Signature perks cheaply.

What about Crypto.com Card, Binance Card, Coinbase Card?

These come up in every comparison search, so here’s the short version.

These are exchange ecosystem cards — they exist primarily to deepen your engagement with a trading platform. Rewards come from staking the platform’s native token (CRO for Crypto.com, BNB for Binance, etc.), which means your cashback is fundamentally a function of how much capital you’re willing to lock up in a volatile exchange token.

- Crypto.com Card can offer up to 5% cashback in CRO — but you need $50,000+ CRO staked to hit higher tiers. For someone willing to lock up that capital and bet on CRO’s price stability, it can outperform Wirex on rewards. For most users, it doesn’t.

- Binance Card is similar but with BNB and is unavailable in many regions.

- Coinbase Card is the simplest of the three (1-4% cashback in selected crypto, no staking), and is the right answer for US users since Wirex doesn’t operate in the US.

If you’re already deeply integrated into one of these exchanges’ ecosystems, their card is a logical add-on. If you’re not, Wirex/KAST/Avici give you crypto card functionality without requiring you to dump capital into a single exchange’s native token.

I’ll publish a full head-to-head comparison covering all of these cards separately. For now, this overview should give you the lay of the land.

Frequently Asked Questions

Is Wirex safe?

For active users with current verification, Wirex has operated since 2014 with no major security breaches affecting user funds. The platform is licensed by the UK’s FCA for limited activities and operates under EU regulatory frameworks in EEA. That said, it’s a custodial platform — Wirex holds your crypto. Standard custodial risk applies. Keep only what you actively spend on the card, store long-term holdings elsewhere.

What happens to my crypto if Wirex shuts down?

This is the risk with all custodial platforms. In theory, regulated providers have safeguards (segregated client funds, insurance schemes in some jurisdictions). In practice, recovery from a shutdown can take months and isn’t guaranteed to be full. The Trustpilot reviews mentioning “defund process taking weeks” relate to account closures, not platform shutdown — those are different situations. Best protection: don’t hold significant balances on Wirex (or any custodial crypto card).

Can I use Wirex in the US?

No. Wirex doesn’t currently operate in the United States. US users should look at Coinbase Card or other US-available options.

How long does Wirex KYC take?

For users with clean documentation (passport, address proof, selfie), automated KYC typically completes within 5-30 minutes. Manual review (triggered by document quality issues, region flags, or random checks) can take 1-5 business days. Users with passports from sanctioned or high-risk jurisdictions should expect longer review times and additional document requests.

Is the 8% cashback worth subscribing to Elite for?

Almost certainly not for most users. The Elite plan costs $29.99/month ($360/year), requires substantial WXT staking, and caps your cashback at 10,000 WXT/month (~€22 at current prices). You’d need to spend ~€275/month on the card at the full 8% rate just to break even against the subscription fee — and you’d cap out at €22 cashback regardless. The math only works if you have very specific spending patterns and don’t mind being WXT-exposed.

Should I worry about the 1.3 Trustpilot rating?

You should be informed by it, not panic at it. The 1.3 rating reflects two real but specific issues: a mass re-verification wave that locked many dormant accounts in 2024-2026, and slow “defund process” for closed accounts (weeks to months to return funds). I went through the re-verification myself, submitted current documents within 24 hours, and my account stayed active with no disruption. For active, currently-verified accounts used regularly, the experience is closer to mine — uneventful and functional.

Can I convert WXT to USDT without leaving the Wirex app?

Yes. Open the WXT balance in the app, tap Exchange, and convert directly to USDT (or any other supported asset). The spread on this conversion is small (~0.5%). This is how I personally handle WXT cashback — convert to USDT periodically, spend USDT or transfer out as needed. Removes long-term WXT exposure.

Are there real alternatives to Wirex if I don’t want a Crypto.com or Coinbase card?

Yes — KAST Card (stablecoin-focused, 170+ countries, custodial, token launch upside) and Avici Card (self-custodial, no rewards but Visa Signature perks for $30/year) are the two I personally use alongside Wirex. Bleap Card is another self-custody option worth considering. See the “Where Wirex Stands” section above for honest comparisons.

Final Verdict

After 5 years of personal use:

Wirex Standard is the best free zero-FX travel card with crypto integration I’ve used.

Not the highest cashback. Not the flashiest app. Not the strongest rewards. But the most boringly reliable card in a category where reliability matters more than peak-rate marketing.

If your decision criteria are:

“I want maximum cashback” → Skip Wirex Standard. Look at KAST higher tiers or exchange cards like Crypto.com with stake.

“I want self-custody” → Skip all custodial cards. Look at Avici or Bleap.

“I want a free card that doesn’t punish me on FX fees, integrates with crypto, and just works abroad” → Wirex Standard is one of the strongest options in 2026, and the one I’d personally pick again.

My rating

7/10

Points held back for the cashback theatre, modest cash withdrawal limits, custodial nature, and the recent compliance friction affecting dormant accounts. Points earned for five years of zero-issue daily use, free pricing, 0% FX, and the kind of multi-region availability that competitors haven’t matched.

If you’re going to apply, do it cleanly: complete passport KYC immediately, verify your address, use the card monthly. That pattern has worked for me, and it’s the pattern that minimizes friction with Wirex’s current compliance stance.

This review reflects my personal experience as a Wirex Standard user since 2021. Fee schedules and limits cited are accurate as of May 2026 for the EEA region, sourced directly from the Wirex app and official Wirex documentation. Limits vary by region — verify your specific region’s terms before applying. This article contains affiliate links — if you sign up via my link, I may earn a small commission at no additional cost to you. This doesn’t change my opinion of the card, which is based on 5 years of personal use before any affiliate relationship.